A number of themes became clear in August, themes that will drive and impact the Toronto and area residential resale market for the remainder of this year and no doubt into 2022.

The first and most important is supply. In August only 10,609 new properties came to market. This contrasts sharply with the 18,599 that came to market in 2020. What is even more shocking is that at the end of August there were only 8,201 properties available to buyers, a 51 percent decline from the same period last year when buyers could choose from 16,662 properties. Available properties were reduced to their lowest level in over a decade. A chronic problem has now become critical.

The critical nature of the supply problem is glaringly evident in certain sub-sectors of the marketplace. At the end of August there were only 337 semi-detached properties available for sale in the entire greater Toronto area. This number is shocking but becomes eye-popping when it is remembered that in August 750 semi-detached properties were reported sold. That means that we enter September with 55 percent fewer semi-detached properties available for sale than the total number reported sold in August. Only the City of Toronto’s central districts have more semi-detached properties available at the beginning of September than sold in the month of August, and only marginally at that.

These numbers make it clear that during the current election campaign, the only housing item on all parties platforms should be supply! Platforms that speak to making purchasing properties easier – ie. longer amortization periods, government assisted loans, reducing mortgage insurance premiums, tax free home buying savings accounts – are misleading at best and reckless at worst. They are blatant, unhelpful, self- serving promises that hope to pave the way to being elected. Supply and ways to achieve it should be the only words uttered by politicians at this time.

The second theme that emerges is the disparity between the 905 region marketplace and the City of Toronto (416). The pandemic and its impact on the house buying consumer has been dramatic. Before the pandemic house prices (on average) were lower in the 905 than in the City of Toronto, nor did house prices rise as quickly in the 905 region. That has all changed.

In August the average sale price for the 905 region was more than $1,050,000. In the City of Toronto it was $1,000,000. Prior to the pandemic these differences were reversed. Also, the increase in average sales prices was more startling in the 905 region than in the City of Toronto. In the 905 region detached properties increased in value by 26 percent, semi-detached by 21 percent, townhomes by 20 percent and even condominium apartments increased by almost 15 percent. By contrast in the City of Toronto detached properties only increased by 11 percent, semi-detached by 4 percent, townhouses by 8 percent, and condominium apartments sales prices by 7 percent.

The explanation is three fold. Firstly there is less supply in the City of Toronto, except for condominium apartments, house prices are still pricier in the City of Toronto, and the pandemic, which has intensified the need for space and safety, coupled with the ability to work remotely, has driven buyers to the suburbs and secondary markets.

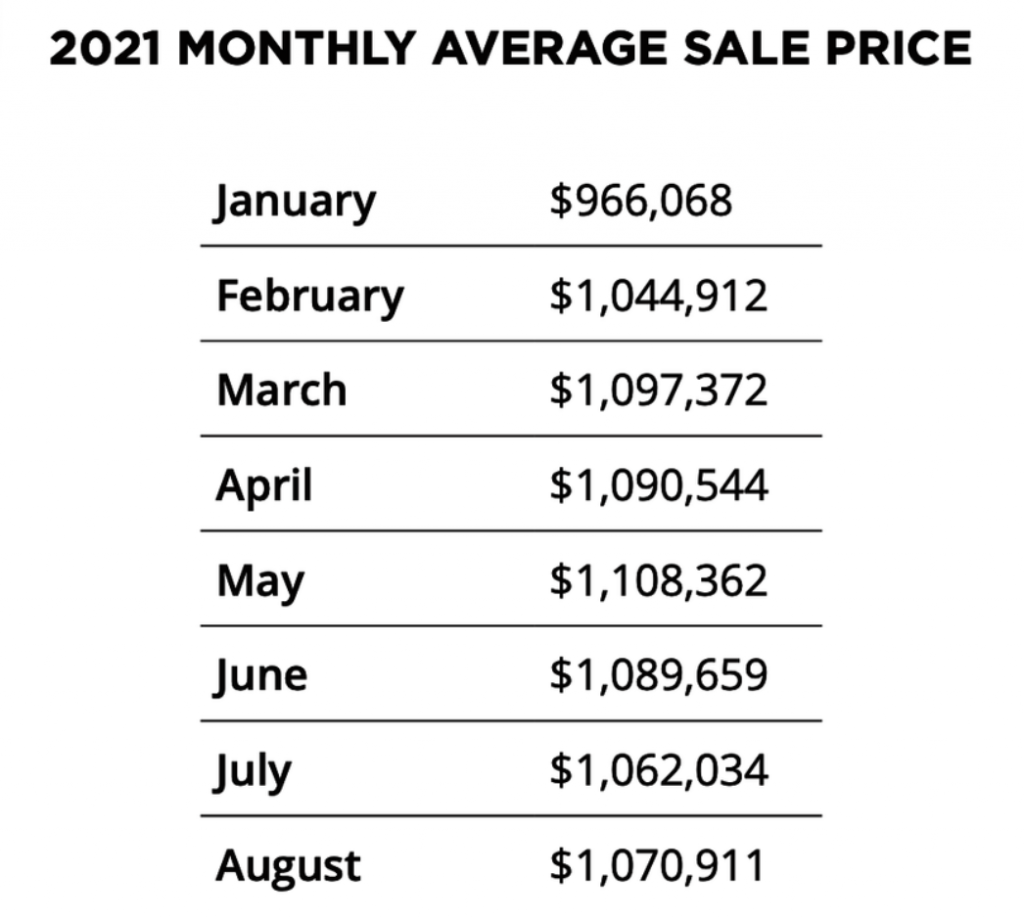

The third theme that has emerged is the plateauing of average sale prices. Yes, August’s average sale price of $1,070,911 for all properties sold was 12.6 percent higher than the average sale price achieved in August 2020 ($951,219), but it has steady declined since May’s stratospheric record breaking average sale price of $1,108,362 and has stabilized at approximately $1,073,000.

Without a mortgage interest rate decline, which is unlikely, or massive increase in household incomes, also unlikely, consumers have reach their maximum housing purchasing power, outliers excluded.

The last theme that is emerging is the resurgence in condominium apartment sales. During the early months of the pandemic condominium apartment sales and prices collapsed. The density of condominium living and fear of the Covid-19 virus drove consumers to ground level properties, especially in the suburbs and secondary markets. Not only were properties less expensive in the 905, and in secondary markets, those prices got consumers more space and the psychological benefit of safety.

August’s results have made it clear that the condominium apartment market is back. In the City of Toronto condominium apartment sales increased by more than 13 percent. Almost 1,740 apartments traded hands, representing almost 58 percent of all properties reported sold in the City of Toronto in August. All condominium apartment sales took pave in only 21 days at 102 percent of their asking price. In Toronto’s central districts, where most sales take place, the average sale price came at $783,712, a number beginning to exceed pre-pandemic levels. Not only are condominium apartment sales robust, but on the supply side they are practically the only game in town. At the end of August, there were 3,577 condominium apartments available to buyers. This, shockingly, represents 44 percent of the total available supply of 8,201 properties of all types.

These themes – supply, disparity between the 905 and City of Toronto marketplaces, the stabilization of average sales prices, particularly in the City of Toronto, and the resurgence of the condominium apartment market – will play out in September, similarly to how they did in August. The result will be sales results and average sale prices similar to what were achieved in August.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.