There were no surprises as to the market’s performance in July. There has been a consistent improvement both as to sales volumes and average sale prices since January. July saw the most dramatic year-over-year improvement. As compared to last year, sales volumes in the greater Toronto area increased by 18.4 percent, and the average sale price was 4.8 percent stronger than the average sale price last July.

In July 6,961 residential resale properties were reported sold in the greater Toronto area. Last year only 5,869 properties were sold. The average sale price came in at $782,129 as compared to $745,971 last July. The average sale price in the city of Toronto came in at $824,336, almost 6 percent higher than the greater Toronto average, notwithstanding that the bulk of the property sales responsible for this average sale price were condominium apartments.

For the first time since the introduction of the Ontario Fair Housing Plan measures, every housing type saw price increases as compared to last year, including detached properties. The average sale price for detached properties came in at $ 1,350,700, an increase of 3.6 percent. Semi-detached properties increased by 7.4 percent to $935,300, and condominium apartments continued their upward trajectory, coming in at $582,247, an increase of almost 10 percent. The average sale price for condominium apartments in Toronto’s central districts, where most sales take place (65 percent), came in at $653,137. Translated as the cost for space, central district condominium apartments are now selling for approximately $1,000 per square foot.

July also saw a recovery in the high-end of the market. The high-end of the market, primarily single-family properties, was dramatically impacted by the implementation of the 15 percent foreign buyer’s tax, the new mortgage stress testing, and three rate increases implemented by the Bank of Canada. For example, during the first 7 months of 2018, realtors reported that 1,247 properties having a sale price of $2 Million or more had sold. This number compares very poorly with the 2,625 similar properties that were reported sold over the same period last year, a negative variance of well over 50 percent.

In July this negative pattern was reversed. In July 181 properties having a sale price of $2 Million or more were reported sold. All but 16 of these properties were either detached (160) or semi-detached (5) properties. This compares favourably to the 149 similar properties that sold in July of last year, an increase of 21 percent. It should be noted that this improvement in sales volume is due to a combination of buyers adjusting to the various measures introduced by governments, increased mortgage rates and sellers accepting that their expectations as to the ultimate sale price of their properties had to be lowered. This is reflected in the fact that the average sale price came in at only 98 percent of asking price for detached homes, and in districts where Toronto’s most expensive properties are located, at only 96 percent. Even these figures are not entirely representative since they do not account for any price reduction from the original list price of these properties.

Inventory levels are a concern. Throughout 2018 they have been declining, particularly in the 416 regions. Of special concern are semi-detached properties and condominium apartments. In both categories, levels are now lower than they were last year at this time. In July there were only 329 active semi-detached properties available to buyers in Toronto, and only 2,583 condominium apartments. Last year there were 2,710 available and that figure was substantially less than the prevailing buyer demand. Due to these shortages, all semi-detached properties sold at 103 percent of their asking price. All condominium apartments sold at 100 percent of their asking price.

Going forward the lack of inventory (semi-detached and condominium apartments) will continue to put upward pressure on average sale prices, but that pressure will be limited. The increase in mortgage interest rates and the implementation of the new mortgage stress testing will limit buyers’ ability to stretch to higher prices as was the case last year. What should result is moderate increases in average sale prices and the number of residential resales. Increases should not exceed 3-5 percent until either interest rates decline, or we see substantial increases in wages and salaries.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

Nasty year over year comparisons came to an end in June. For the first time in more than a year, we saw positive variances in the number of sales and average sale prices. It was unrealistic to compare the first few months of 2017 to any period. Those months represented the most frenetic period in the history of the Toronto residential resale market, even more, dramatic than Toronto’s last frenetic increase in real estate prices in the late 1980’s. Last year’s collective market psychosis was fueled by historically low-interest rates, demand that exceeded supply, and an unrealistic belief that house prices would never stop rising. When the Ontario Fair Housing Plan measures were introduced in late April, it was the electric shock that woke up the psychotic market. What the government’s measure couldn’t impact was demand. With a large number of people migrating to the greater Toronto area annually and the limited amount of new supply available to buyers, demand will always remain strong. It’s not surprising therefore that the residential resale market produced such strong numbers in June.

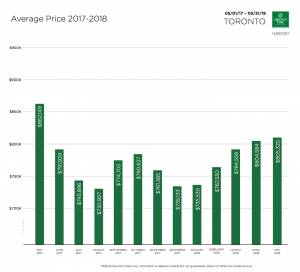

During the month of June 8,082 properties were reported sold. This compares favourably with the 7,893 properties sold last year. It was not surprising that the average sale price also popped in June. In June the average sale price came in at $807,871 a 2 percent increase compared to the $791,929 average sale price last year. As the chart below indicates, the average sale price for all properties sold in the greater Toronto area has been making a steady recovery since the beginning of this year.

Demand and supply will continue to play significant roles going forward. It is troubling that only 15,922 properties came to market in June. Last year 19,561 properties came to market, a decline of almost 19 percent. Although active listings at the end of June were on par with the number available to consumers last year, most of that inventory represents the residue of the market build-up following the implementation of the Ontario Fair Housing Plan.

What the average sale price belies is the fact that it was achieved notwithstanding that the high-end of the market continues to lag. In June 237 properties were reported sold having a sale price of $2 Million or more. Last year 264 were reported sold over the same period. On a year to date basis, 1,067 properties in this price category have been reported sold, a stunning reversal from the 2,483 that sold last year. June’s results are, however, encouraging, and as continued positive variances are produced through the balance of 2018, the higher-end will begin participating equally with the rest of the residential resale market.

The long-term problem will become affordability. Average sale prices are starting to inch towards the numbers that prompted the Liberal government to implement the 15 percent foreign buyers tax. In the city of Toronto, the average sale price for all properties sold was $870,559, approximately 9 times the average household annual income. The resilience of the Toronto and area market makes it clear that if there is insufficient supply, and growing demand, no amount of government engineering will make housing more affordable. It will take a collective political will at the municipal, provincial and federal levels to address the supply issue. Unfortunately, we have seen no collective initiative in this regard.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

There were no surprises in the May resale figures for the Toronto and area residential market. The three themes that emerge are that the city of Toronto resale market continues to strengthen (416 regions); the 905 region continues as a drag on the overall market, and the high-end of the resale market ($2 Million plus) has yet to return to anywhere near its early 2017 performance.

The City of Toronto has almost returned to the way it was performing last year. The average sale price for all properties came in at $861, 970. Last year at this time it was $899,000. The number includes condominium apartment sales which, significantly, continue to represent the most affordable housing available in Toronto, and accounted for more than 56 percent of all properties reported sold in May.

All properties (including condominium apartments) sold in only 16 days, and impressively, sold for 101 percent of their list price. In the eastern districts located closest to the central core (Riverdale, Leslieville, Beaches) all properties sold in just over 8 days, at more than 110 percent of their asking price. These are some remarkable statistics that are generally ignored by the daily newspapers and articles related to the Toronto and area marketplace.

The data immerging from the 905 region is not as impressive. Notwithstanding the size of the 905 region, only 60 percent of all reported sales (7,834) took place in the region. The average sale price of $805,320 was more than $55,000 lower than the average sale price of $861,970 achieved in the City of Toronto.

What is troubling about the 905 region is that 73% of all available inventory is located in the region. In May there were 20,919 properties available to buyers, but only 5,797 in the City of Toronto. As a result, the sales to list ratio in Toronto was 56.5 percent, but only 46.8 percent in the 905. The months of inventory in the 905 is 2.6, while only 1.9 in Toronto. All sales in the 905 took place in 20 days, but only 16 in Toronto, and not surprisingly, all sales in the 905 took place at 99 percent of their asking price, but at 101 percent in Toronto. Given this discrepancy in market performance, it becomes extremely deceptive if the Toronto and area resale market are analyzed as a whole, and not as two distinct marketplaces.

In May 233 properties having a sale price of $2 Million or more was reported sold. This compares very poorly with the 427 similar properties reported sold in May last year. This represents a 45 percent reduction year-over-year. The explanation for this decline is many-fold. Last year, on the obsessive belief that house prices would continue to skyrocket, high-end average sales prices reached unsustainable levels. Since then there have been three mortgage interest rate hikes, and banks are now applying more restrictive stress testing on all properties. The 15 percent of foreign buyers tax is playing some role in this scenario, but less significant than the provincial government’s perception.

All of these factors have had a strong psychological impact on buyers. They are clearly waiting to see if prices will continue to fall at the high end. That hesitation has resulted in the sharp drop in sales in this price category. However, as May’s results for the City of Toronto indicate, the market is improving which will have an ameliorative impact on the psychological hesitation of buyers in this price category.

Inventory levels are becoming a concern, particularly in the City of Toronto. Last year there were 5,779 active listings at the end of May, a period of severe inventory shortages. This year there are only 5,797. Although the difference is marginal, it represents a pattern that has been emerging. Declining inventory will lead to rising prices and hyper-competition for good properties in desirable neighbourhoods.

Condominium apartment inventory is also declining. Last year there were 2509 active listings at the end of May. This year there are 2552. Again, the difference is insignificant but a declining pattern is emerging. This is very concerning because condominiums apartments remain the most affordable housing in Toronto, at least for the time being. Prices for condominium apartments have been increasing. The average sale price for condominiums apartments in Toronto is now $602,000 and a stunning $671,000 in the central core. Considering that 64 percent of all apartment sales in Toronto are in the central core, affordability is now becoming a concern, even for condominium apartments.

Looking forward to June, it’s possible to see a marketplace that once again can be favourably compared to last year. The initial impact of the Ontario Fair Housing Plan measures will be history and next month’s chart will look much smoother than the one below:

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

The Toronto and area residential resale market continued its recovery in April. For the fourth consecutive month, the market has shown improvement in both the growth of average sale prices and the number of properties reported sold. In April 7,792 residential properties were reported sold, and the average sale price for all properties reported sold in the Greater Toronto Area came in at $804,584. In January, the average sale price had slumped to $735,754. In four months, Toronto’s average sale price has increased by almost 10 percent.

The market has not recovered to where it was in April 2017, but it is showing signs that it might, particularly in the City of Toronto (416 region). The reason for this recovery is obvious. The fundamentals that drove the frenzied early 2017 resale market are unchanged: strong employment numbers, a growing economy, migration to the greater Toronto area, and insufficient inventory to meet buyer demand. With more than 100,000 people migrating to the Toronto area annually, the supply-demand scenario is no longer in balance. It’s a testament to the strength of the Toronto resale market that it has continued to recover notwithstanding three mortgage interest rate hikes and new more rigid stress testing for mortgage qualification.

In the City of Toronto, the average sale price came in at $865,817 for all types of properties sold, including condominium apartments. The cost of a detached property rose to $1,354,719, while semi-detached homes came in at $1,021,986. These numbers are starting to approach the numbers that the market was producing last year. Year-over-year sale volumes are down by 34 and 16 percent respectively, but in the case of semi-detached properties, this is a product of supply and not demand. In some of Toronto’s trading area, there were no reported sales of semi-detached properties. That’s because there were no listed properties for buyers to buy.

The strength of the market is profoundly demonstrated by the short time periods that detached and semi-detached properties remained on the market. All detached properties sold in only 17 days and for an amazing 101 percent of their asking price. All semi-detached properties sold in an eye-popping 13 days and for a startling 106 percent of their asking price. These numbers are only slightly short of what was happening last year.

Condominium apartment prices have risen consistently, even through the downturn in the market following the announcement of the Ontario Fair Housing Plan in April of last year. In April, and for the first time, the average sale price for all condominium apartments sold exceeded $600,000 coming in at $601,211. In Toronto’s central core, where more than 67 percent of all sales take place, the average sale price reached $667,345. Toronto’s most affordable housing form is rapidly becoming less affordable. Not only did condominium apartments sell with growing average sale prices, but they all sold in only 16 days and at 101 percent of their asking price. In the central core, they also sold at 101 percent of their asking price and in only 15 days.

Condominium Apartment sale prices are, like other housing forms, being driven by a severe lack of supply. At the end of April, there were only 2,130 apartments available to buyers, a little more than one month’s supply. Last year at the height of Toronto’s frenzied market there were 2509 condominium apartments on the market, a year-over-year decline of available inventory of more than 15 percent.

The high-end market has been the only laggard in Toronto’s resale market. Year-to-date only 600 properties having a sale price of $2 Million or more have been reported sold. Last year 2221 had been reported sold, a decline of more than 73 percent. This market sector is, however, also improving. In April the negative variance, as compared to last April, was only 48 percent.

The Toronto and area marketplace is beginning to send out two powerful messages. Firstly, the foreign buyer’s tax that was part of the Ontario Fair Housing Plan was directed towards a non-existent enemy. There were no hordes of foreign buyers buying Toronto real estate. There were no barbarians at the gate. That has been subsequently verified by not only the provincial government but by other sources, namely the Toronto Real Estate Board and CMHC. Secondly, the Toronto resale market is being driven by local, domestic forces. That being the case, governments should abandon any attempt to engineer the marketplace and focus on measures that will help the increase of supply.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

In March the Toronto residential real estate market clearly demonstrated its resilience. Notwithstanding the provincial government’s attempt to engineer the market, it continues to respond to forces that have nothing to do with the Ontario Fair Housing Plan. That’s due primarily to the fact that the underlying basis for the province’s measures, namely foreign buyer speculation, were unfounded. Since the implementation of the Fair Housing Plan, it has been demonstrated that less than 5 percent of all purchases of residential properties in the greater Toronto area involved foreign buyers.

The real and fundamental factors driving the Toronto and area marketplace have remained unchanged: low unemployment, rising wages, a growing (albeit modestly) economy, and most importantly, the combination of low supply and continuous immigration into the greater Toronto area. Ultimately what will control the Toronto residential marketplace is the market itself, specifically the cost of housing. The Fair Housing Plan, to its credit, did act as a wake-up call to buyers, but ultimately it will be the cost of mortgage money, qualifying for mortgage financing, rising average sale prices (due primarily to a lack of supply) that will control and moderate the residential resale market.

In March the lack of supply was clearly demonstrated by the rising average sale price. March saw an average sale price for all properties in the greater Toronto area of $784,558, an increase of 2.2 percent compared to January, and almost 7 percent higher than February’s average sale price. Demand was demonstrated by how quickly all listed properties sold in March. The average days on market was only 20. That is a pace consistent with the most aggressive seller’s market. In some areas of the market, particularly in the 416 region, the days on market was even lower.

All detached properties in the 416 region (City of Toronto) sold in only 17 days. All semi-detached properties sold in a shocking 13 days, and in only 11 days in Toronto’s eastern regions. All condominium apartments in the City of Toronto sold in only 17 days. As hard as this is to believe, this is a pace not that different from the delirious pace of the first four months of 2017.

When the market moves at the above-noted pace, it is not surprising to see average sale prices rising. In the City of Toronto all properties, including condominium apartments, sold for 101 percent of their asking prices, coming in at $817,642. All detached properties sold for 100 percent of their asking prices, coming in at almost $1,300,000. Unbelievably semi-detached properties sold for 107 percent of their asking prices, the average sale price exceeding $1,000,000. Even condominium apartments sold for 101 percent of their asking prices with an average sale price of $590,000. In Toronto’s central core, the average sale price for condominium apartments was $656,836, not that much less than average sale price for all property sales in the greater Toronto area. Condominium apartment sales are now taking place at approximately $1,000 a square foot.

The ultimate reason for these incredible numbers is the lack of supply. Notwithstanding that the number of active listings in March (15,971) was 103 percent higher than the 7,865 properties available last year, the bulk of the available listings are located in the 905 region. Of the 15,971 available properties for sale, 75 percent are located in the 905 region. In the case of detached properties, 83 percent of all detached properties are located in the 905 region. The situation involving condominium apartments is reaching crisis proportions. In March 1,573 condominium apartments were reported sold. At the end of March there were only 1,854 condominium apartments available for sale, most of them in Toronto’s central core. If this rate of absorption continues, there will be almost no product for buyers. This is particularly troubling because condominium apartments have been the only affordable housing type available to buyers.

Detached properties were the only housing type that continues to lag behind the rest of the Toronto market. Sales were off, year-over-year, by more than 40 percent, and average sale prices were o by almost 18 percent. The explanation is self-evident. During last year’s delirious market, mortgage money was historically cheap and relatively accessible. Since then not only has mortgage money become more expensive – three bank rate hikes in the last year – but new mortgage stress testing for conventional mortgages makes qualifying substantially more difficult. It should also be noted that during the January through April real estate madness of last year’s average prices reached astronomical levels, levels that simply could not be sustained.

Going forward we are not likely to see much change in Toronto’s residential resale market. The key to change is more supply. There is no indication either at the provincial or municipal level that measures will be taken that would have a positive impact in this area. For political reasons governments may attempt further engineering, but any such actions will have a limited impact on the market, but are likely to have broader, negative economic impact. Without dramatic change to Toronto’s available supply, Toronto will become one of many other cities in the world that because of their political and financial stability where real estate ownership will not be available to everyone. That begs another question: what about the rental supply?

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

There were no surprises in February’s residential resale data.

Last year in February the market was verging on delirium. With record low mortgage interest rates, a severe supply problem, and a collective psychological belief that if you didn’t buy immediately you would be shut out of the market permanently. Under these conditions it was not surprising that prices were increasing by more than 30 percent on a year-over-year basis.

Its also not surprising that this year we are witnessing negative variances as compared to last year. Since the early months of last year, we have seen government intervention in the form of three mortgage rate hikes, a 15 percent foreign buyers tax, and a rigid new form of stress testing borrowers seeking conventional mortgage loans. Conventional loans are mortgages that do not exceed 20 percent of the value of the property. Yet despite all of this the Toronto and area residential resale market has held up fairly well.

There were 5,175 reported sales in February, a 34 percent decline compared to the 7,955 sales reported last year. But comparing this year’s sales against last February is like comparing the Toronto market against a fictional metropolitan area that no longer exists. Last year’s results were extraordinarily driven by a never before seen market delirium, a delirium that crashed with the announcement of the provincial government’s Fair Housing Plan and the implementation of the foreign buyers tax.

Yet despite all these market shocks, all properties still sold in only 25 days and the average sale price in the greater Toronto area came in at $767,818, a 12 percent decline compared to last February. That decline, however, requires some clarification. The decline in average sale price was primarily driven by the decline in sales and prices in the 905 region and the decline in sales of higher priced properties ($2 Million or higher). The average sale price in the City of Toronto (416 region) came in at $806,494 and that despite the fact that the bulk of all condominium apartment sales——- the least expensive housing type———are located in the city of Toronto. Prices in the 905 region declined to $767,816, a substantial decline from last year when they came In at $876,000.

The biggest drag on average sale prices was the decline in higher priced property sales. This is not surprising and expected. In last year’s frenzied market, 389 properties sold having a sale price of $2 Million or more, most of them being detached properties. This February only 126 properties in this price point were reported sold, a 67 percent decline. A decline of this magnitude, representing more than 5 percent of the entire market, will have a powerful, negative impact on the market’s average sale price.

Again it is not surprising that this decline has occurred. Detached property values had reached stratospheric, unsustainable levels. Last year the average sale price for a detached property was approaching $1,600,000 for the greater Toronto area and more than $2,500,000 in Toronto’s central districts. This year average sale prices have been reduced to $1,282,240 and $2,027,761 respectively. These are prices that are beyond the reach of most buyers, particularly with the increase in mortgage interest rates and the new stress testing. Given the impact of these factors we can anticipate further softening of prices for sales of this property type, or at the very least a plateauing.

Semi-detached sales are also in decline compared to last year but to a lesser degree and for different reasons. Across the city of the Toronto the average sale price for semi-detached properties still came in at $985,902, and at more than $1,235,000 in Toronto’s central districts. Sales of all semidetached properties took place in only 19 days and at 103 percent of their asking price. These are not statistics emerging from a market that is in trouble but rather the opposite. In Toronto’s eastern districts, particularly those closest to central Toronto, all sales took place in only 13 days and for sale prices approaching an astounding 110 percent of the asking price. These numbers point to strong demand and a very limited inventory.

The supply of resale condominium apartments is approaching crisis levels. In February 1,687 new condominium apartment listings came to market, a 10 percent decline in the number of listings that came to market last year. The Toronto condominium market effectively finds itself in exactly the same position as last year at this time, except that prices are almost 11 percent higher. The condominium apartment that one could buy last year for $515,000 will now cost buyers $570,000. In the central districts where most buyers would prefer to locate, the average sale price is now an amazing $645,000. Last year the average sale price was $ 577,000. All condominium apartments sold on only 22 days and for 100 percent of their asking prices. Ironically in Toronto’s central districts, where prices are highest, all condominiums apartments sold in only 21 days and for 101 percent of their asking prices.

The Toronto and area marketplace is where it would have been without the provincial government’s intervention, constrained by the weight of, what is now clear, unsustainable prices. Going forward sales will pick up as sellers come to the realization that except for the most desirable properties in the most desirable areas, sale prices achieved last year are no longer realistic, particularly with higher mortgage interest costs. Basic economic factors——employment, strong economy, increasing wages——are very positive and therefore demand will remain powerful. When prices align with buyers’ financial capabilities the market will once again begin to grow, but prices will remain in check, especially if we see further increases in mortgage interest rates, as anticipated.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.