If you’ve been considering buying or refinancing any time soon, you may have come across the term “Stress Test” and wondered what is a stress test and why does it matter to you.

We aren’t talking about a medical stress test, although many of us may need one if the home prices keeps rising at the rate they have been, we are talking about a mortgage stress test which can affect your ability to purchase the home you’ve fallen in love with. With Toronto real estate prices as high as they are and at the speed in which they are rising at the time of this blog post (February 2022), it is important to understand what a stress test is and how it applies to you when making a move. Below is a detailed explanation as to what a stress test is and how it can affect your purchasing power.

What Is Stress Test:

Because mortgage rates can fluctuate, as of 2016, the Canadian government introduced a minimum qualifying rate in order to reduce the risks associated with mortgage lending. This qualifying rate ensures that you are still able to cover your mortgage payments even if rates rise above your original qualifying rate as the qualifying rate is higher than your contract rate with your lender. This rate is based on a number of factors including your current credit score, credit history, total amount being mortgaged, current debts and your income.

How A Stress Test Works:

When you apply for a mortgage with a lender, your lender will provide you with a contract rate which is based on current interest rates, your credit history, the structure of your mortgage and current economic factors at the time of your application. Although your lender will provide you with a contract rate, they are required to qualify you first at a higher qualifying rate in order to ensure that you could cover your mortgage payments even if rates rise. This process is simply a risk assessment for your lender.

Why The Stress Test Was Introduced:

The test was introduced in 2016 when the Toronto real estate market was thriving and when homeowners were taking on substantial household debt. The test was originally only required for insured mortgages (a mortgage that includes mortgage default insurance) and with less than a 20% downpayment. The main goal of introducing this test was to provide both the lenders and homeowners with a buffer should anything happen that would increase the interest rate or monthly payments. The Canadian Government later extended this test requirement to uninsured mortgages as well (mortgages without default insurance and with more than 20% down). Not only does this test affect those who are applying for their first mortgage but also those who are looking to refinance.

How Does The Stress Test Affect Borrowers:

Due to the fact that borrows need to be approved on a higher rate than the contract rate, some buyers (depending on their financial situation) will have reduced buying power and may have to settle for a home at a lower price point. This can make the buying process somewhat frustrating if you aren’t able to find a property that fits your needs.

One positive aspect of the test is that you as the buyer know you won’t be over extending yourself financially.

Can You Avoid A Stress Test:

Unfortunately, you cannot avoid a stress test as all major banks and lenders are required by law to complete stress tests on their borrowers.

How To Calculate What You Can Afford Based On The Stress Test:

The Government of Canada has created a mortgage stress test calculator which allows you to calculate what you can afford based on the test. You can access the calculator HERE to determine how much you can be approved for based on your specific information and circumstances.

It’s very important that you always speak with your lender and get pre-approved before submitting an offer on a property in order to avoid running into any financial hiccups.

Are you thinking about making a move and have questions? Contact me any time, I’m always happy to help.

There were a few surprises and once again a number of new records established by the Toronto and area residential resale market in January.

First, and very noteworthy, was the average sale price for all properties reported sold. It came in at an eye-popping $1,242,793, surpassing the previous record of $1,163,210 achieved in November of last year. By contrast, last January the average sale price came in at only $966,068, a year-over-year increase of almost 30 percent. This is not supposed to happen in January, historically a quiet month, and it happened during a snow filled month making access to properties extremely difficult.

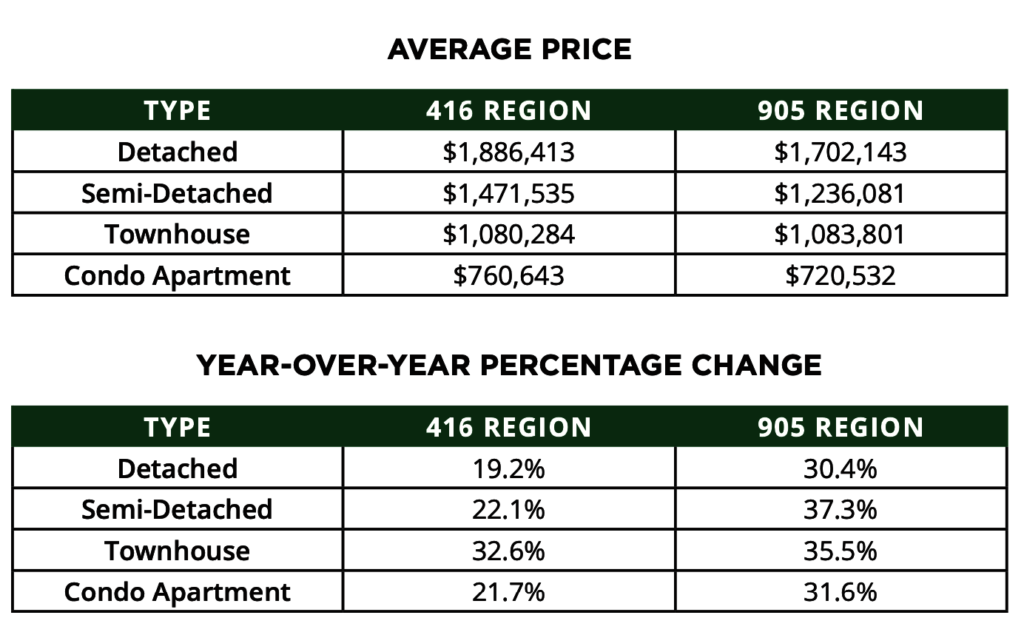

As has been the case throughout the pandemic, the increase in the Toronto and area average sale price was 905 driven. As the chart below indicates, year-over-year price increases in Toronto’s 905 region averaged almost 34 percent and only 24 percent in the City of Toronto.

As a result of these increases, the 905 has dramatically reduced the gap in housing prices between the City of Toronto and the 905 region. With more people working from home and needing more interior and outdoor space, this pattern will continue throughout the foreseeable future.

A trend that began in the second half of 2020 has now become common place, namely the disparity between list and sale prices. Throughout the entire Toronto and area marketplace all properties sold for 113 percent of their asking price, including 2016 condominium apartments. The most startling disparity was the reported sale of semi-detached properties in Toronto’s eastern districts. All semi-detached properties throughout the eastern districts sold for 127 percent of their asking price, and astoundingly in the neighbourhoods of Riverdale and Leslieville the sales to list ratio was 134 percent, another market record, and a buyer’s nightmare. This discrepancy will only get worse. At the beginning of February there were only 26 active semi-detached property listings for the entire eastern trading area.

The luxury market has also undergone a major transformation over the past few years. In January, 590 properties were reported sold with a sale price of $2 Million or more. This compares with only 331 in January 2021, 130 in 2020, and a mere 76 in 2019 – a 676 percent increase in three years. This is also, no doubt, a record. Clearly the definition of “luxury” will have to be redefined.

The other end of the market spectrum, condominium apartment sales, continue to increase in price. A year ago, condominium apartment sale prices in the city of Toronto resulted in a negative variance, down 8 percent compared to 2020. This January condominium apartment prices rose by almost 22 percent to $760,643. But the real story is in Toronto’s central core. In January, 966 apartments were reported sold with an average sale price of over $800,000. Considering that central core sales account for almost 70 percent of all City of Toronto apartment sales, what used to be the most affordable housing type is starting to become quite pricey. What’s worse is that in one year the available supply of condominium apartments has declined from 2,360 to 1,095, a 53 percent decrease.

Supply generally will be the driving – rather inhibiting – market force in 2022. Supply was at an all-time low at the end of 2021, with no improvement in January. January saw 7,979 properties come to market, a decrease of almost 16 percent compared to the 9,438 that came to market last year. As buyers venture into the February market only 4,140 available properties await them, a 44 percent decline compared to the 7,396 (also extremely low) available last year.

With this shocking low level of supply, it is not surprising that reported sales were down in January compared to last year. There were 5,636 sales in January, down over 18 percent compared to the 6,888 property sales last year. Notwithstanding this negative variance, it must be remembered that January’s numbers are very robust compared to what used to happen in January before the pandemic. For example, in January 2020, the month that Covid-19 became part of our vocabulary, only 4,546 sales were reported, and the year before that only 3,968.

Looking ahead all eyes are on the Bank of Canada and when it will raise interest rates. Given the level of demand and the lack of supply the impact of higher mortgage interest rates will likely be moderate. Those buyers struggling to qualify today will be forced out of the market, especially first time buyers, but for every one of them there are still many who are intent and capable (if they can find one) on acquiring a house.

Have questions about the market, selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.