In the September Market Report, five themes that were driving the Toronto and area marketplace were identified. These themes have become prominent during the course of 2021 and it is becoming evident that they will be the key features of the residential resale market for the remainder of 2021 and into the early months of 2022. These themes, with slight variation, were prominent in the October market data.

1. AVERAGE SALE PRICE

Prior to October, it appeared that the average sale price for all properties sold had plateaued around $1.1 Million, including condominium apartments. In October the average sale price popped up to $1,155,345 (also including condominium apartments), into record territory, and substantially higher than the $968,535 achieved last year, a 19.3 percent increase year-over-year. What drove this unexpected increase? Another key theme, the tension between market demand and supply.

2. DEMAND-SUPPLY TENSION

The demand-supply problem moved beyond critical into a danger zone in October. In October 11,740 properties came to market. That was 34 percent fewer than the 17,806 that came to market last year. Couple that with the 9,783 properties that were reported sold in October, by month-end there were only 7,750 properties in the entire greater Toronto area for sale. Compare that to the 17,313 that were available last year, and it becomes abundantly clear that we are in a dangerously imbalanced zone.

This imbalance will become even clearer when we discuss what’s happening to sale prices as compared to asking prices. With so little supply, and record levels of demand, the problem of lack of supply and affordability becomes acute. Multiple offers are the norm, no longer the exception, and based on the average sale price for October of $1,155,345, buyers competing for the limited number of properties on the market are driving Toronto and area into one of the most expensive cities on the globe.

3. CITY OF TORONTO V. 905

As 2021 winds down to a close, the disparity between the City of Toronto and the 905 region has been dissipating. Beginning in the late spring of 2020, during the height of the pandemic, more and more buyers have been flocking to the 905 region (and to many secondary markets throughout southern Ontario). As 2021 has unfolded, prices in the 905 region have increased dramatically, proportionally faster than those in the City of Toronto, and more recently, the availability of properties for sale has declined to the point where there are now more properties for sale in the City of Toronto than in all the 905 region.

At the end of October, as mentioned above, there were only 7,750 properties available for sale in the entire Toronto and area region. A closer look indicates that 4,247, or almost 55 percent of those properties were in the City of Toronto. That leaves only 3,503 available properties for sale from Burlington to the west, to Innisfil in the north and to Clarington in the east. This is a vast region. The lack of supply in the 905 region is a product of the pandemic, and buyers’ need and desire to have more space, safety and to satisfy their need for security. The ability to work remotely has fuelled and enabled this diaspora, but now the 905 region is without supply and with startlingly higher average sale prices.

At this pace the difference in price, for all housing types, will evaporate. It’s particularly interesting to note the dramatic increase in suburban condominium apartment prices. *October year-over-year increases.

4. LIST PRICES V. SALE PRICES

In October every trading area saw sale prices come in substantially higher than list prices. For the entire greater Toronto area the average sale prices was 107 percent of the asking prices. This includes all reported sales in Halton, Peel, York, Durham, Dufferin, and Simcoe Counties. Effectively the asking price is a point of commencement, and that’s all. Scarcity, location, demand, and auction style sales, will determine the end price. In various locations the percentage of sale price over ask was even higher. For example, all semi-detached properties in Toronto’s eastern trading areas sold for 115 percent of asking price and in an eye- popping 7 days!

It is not surprising that entering the month of November there were fewer active listings of every type of property, except condominium apartments, than were sold in October. In some trading areas the situation is dire. In the greater Toronto area 878 semi-detached properties were reported sold in October. November begins with only 347 available semi-detached listings. Not much choice for buyers, putting further pressure on both availability and affordability.

5. CONDOMINIUM APARTMENTS

Condominium apartment sales continued their resurgence in October. In the City of Toronto, sales were up by almost 34 percent compared to a year ago. Similarly in the 905 condominium apartment sales were up by almost 21 percent to 986 units. Prices followed the rise in sales, increasing by almost 11 percent in the City of Toronto and by 17 percent in the 905 region. Clearly, buyers have overcome their weariness of living in high-rise towers in more dense conditions, or this simply may be due to the fact that compared to ground level opportunities, condominium apartments remain the most affordable housing type and choice.

Like all other housing types, the supply of condominium apartments is declining. At the end of September, there were 3,882 active condominium listings in the greater Toronto area, and 2,918 in the City of Toronto. At the end of October the supply of condominium apartments throughout the entire region had declined by more than 11 percent to 3,440, and by 7.5 percent to only 2,700 in the City of Toronto. The last bastion of affordability and supply is quickly disappearing.

These five themes will sum up the Toronto and area marketplace for months to come. The now more real, looming threat of mortgage interest rates may cause a disruption to these themes. Based on the Bank of Canada’s recent pronouncements we may see rate hikes within the next few months. Rate hikes will have no positive impact on supply, although they will no doubt curb the rising prices that we witnessed in October.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market, selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

The importance of a good credit score is one of the most important considerations in life. Your credit score can determine whether you can get a loan, how much you will have to pay for that loan, and even whether you can rent an apartment. Your credit score is also a measure of your financial responsibility, so it’s important to understand what it is, how to keep it as high as possible and improve it if it’s currently low. In this blog post, we will discuss what a credit score is, how to get your credit score, what affects your credit score, and how to improve your credit score.

What Is A Credit Score

A credit score is a number that represents your creditworthiness. It is based on your credit history, which is a record of your borrowing and repayment activity.

Why Does Your Credit Score Matter

The higher your credit score is, the more likely you are to be approved for loans with favourable interest rates. Conversely, the lower your credit score, the less likely you are to be approved for loans or favourable rates and terms. Having a low credit score can make your life very difficult as you may not be able to get a mortgage, rent a property, obtain a credit card or purchase a vehicle.

What Is A Good Credit Score

As per Equifax’s website (as of October 2022), a good credit score is typically anything between 660 to 724 and 725 to 759 are considered very good, while anything above 760 is considered to be excellent. Having an excellent credit score can make your life a lot easier when it comes to getting loans along with lower interest rates. You can view Equifax’s explanation of what a good credit score is at the video below.

What Affects Your Credit Score

There are a few things that can affect your credit score. These include your payment history, the amount of debt you have, the length of your credit history, the types of credit you have, and new credit inquiries.

How To Rebuild Your Credit History

If you have a bad credit score, don’t despair. There are things you can do to rebuild your credit history. First, make sure you make all of your payments on time from now on. Second, pay off any debts you have as soon as possible. Third, don’t apply to open new accounts unless you absolutely need to. Fourth, try to get a mix of different types of credit. Finally, don’t apply for new credit too often.

How To Get Your Credit Score

The two most common ways to get your credit report is through Equifax or TransUnion ,these are the two most reputable credit reporting agencies here in Canada. You can request your credit report from Equifax and Trans Union via online, phone, by mail or in person. Additionally, if you have a credit car, you may be able to request a copy of the credit score from your credit card company as some banks and lending institutions have started offering this. Below is a short clip with additional information regarding credit scores and how to access yours.

Bad credit can be a real burden, preventing you from getting loans, renting apartments and buying a home. Keeping a good credit score will ensure that you can avoid such burdens and achieve your objectives whether it be real estate related or otherwise.

Hopefully the above has helped explain the importance of a good credit score.

Are you thinking of making a move? Contact me any time with any questions you may have about buying, selling, leasing or the market in general. I’m always happy to help.

The residential resale market rebounded in September after five months of declines in sales and the lull of the summer months. There were 9,046 sales reported in September, 18 percent fewer than reported last year, but more than 5 percent higher than the 8,580 reported sales in August, the first month-over-month increase since the early spring of this year.

As indicated in our August Report, there are a number of themes that are driving the market, themes that will continue at play for the remainder of this year and into 2022.

1. AVERAGE SALE PRICES

Average Sale Prices for all properties sold have been fairly stable through 2021. The average sale price has been approximately $1,080,000 since February, fairly consistent throughout those months, including the month of March, which saw the market deliver an unbelievable 15,629 sales.

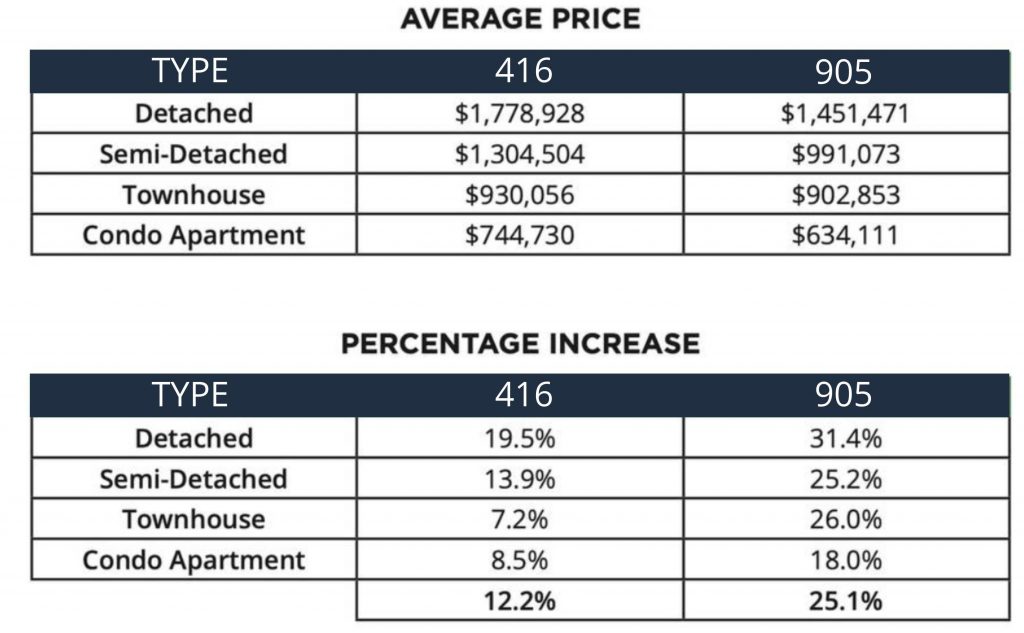

In September, however, the average sale price jumped to a record-breaking $1,136,280: eye-popping because it includes 2,664 condominium apartment sales, which represent 30 percent of the entire market with an average sale price of only $708,000. Needless to say, the average sale price of ground-level property was on fire, with the average sale price for detached and semi-detached properties in the City of Toronto coming in at $1,779,000 and $1,305,000, respectively. The average sale price for the greater Toronto area will continue to rise, primarily by what is happening in the 905 Region.

2. CITY OF TORONTO – 905 REGION DISPARITY

In September average sale prices in the 905 Region once again accelerated much faster than in the City of Toronto, as is illustrated in the chart below.

As measured against all property types, the average sale price increased by more than 25 percent in the 905 Region as compared to only 12.2 percent in the City of Toronto (416).

The reason for this disparity is obvious. House prices of all types remain substantially less expensive in the 905 Region as compared to the City of Toronto, however they are catching up.

3. DEMAND-SUPPLY TENSIONS

September has clearly illustrated that demand, throughout the greater Toronto area, is dramatically high, and unfortunately, supply is chronically and historically low. It was no surprise that affordable housing was a key campaign platform for all parties during the recent national election.

At the end of September, there were only 9,191 available properties throughout the greater Toronto area, almost 50 percent fewer than last year. It is not surprising therefore that all properties that came to market in September (on average) sold in only 14 days, and substantially less in some sub-markets; for example, semi-detached properties in the City of Toronto (only 11 days). What is especially concerning is that the available supply in the 905 Region has dwindled dramatically.

In September of the 9,191 properties available for sale, 52 percent of them (4,821) are located in the City of Toronto. Of those 4,821 available properties, 2,918 are condominium apartments. Historically only 30-35 percent of available properties were located in the City of Toronto, the balance in the 905 Region. There is no clearer evidence that the pandemic has caused buyers to look beyond the City of Toronto, where house prices were less expensive and the supply was more plentiful. Not any more.

4. LIST PRICES VS. SALE PRICES

Except for one trading area in the City of Toronto, where the average sale price was $5,625,720, the recorded sale price of all properties sold throughout the greater Toronto area exceed the asking price, on average by 106 percent. This is a first, and it proves that in this market the list price is merely a starting point. No one expects that the end sale price will be equal to or lower than the asking price. This phenomenon is a product of the demand-supply problem. In some trading areas, the end sale price exceeded the asking price by substantially more than 106 percent. For example, all semi-detached properties in Toronto’s eastern trading areas sold for a breathtaking 118 percent over the asking price.

To reiterate, the list price of properties today is only a starting point.

5. CONDOMINIUM APARTMENT SALES

Condominium apartment sales, devastated by the early effects of the pandemic, have come roaring back, and so have their sale prices. In September 2,664 condominium apartments were reported sold across the region, exceeding pre- pandemic sales numbers. Of those 2,664 condominium apartment sales, 1,792 were in the City of Toronto.

As the chart above illustrates prices are following sales. In the City of Toronto, the average sale price increased to $744,730 and to $634,111 in the 905 Region, 8.5 and 18 percent, respectively. In the central core of Toronto, where 1,176 sales were recorded (44 percent of all recorded sales) the average sale price reached $806,242, a record high and the first time the average sale price has exceeded $800,000. Even Toronto’s least expensive housing type is now becoming pricey.

Going forward the five trends that have been discussed in this Report will continue to influence the resale market. Expect sales in October to be even stronger than September, with continued pressure on sale prices due to the lack of available supply.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market, selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

A number of themes became clear in August, themes that will drive and impact the Toronto and area residential resale market for the remainder of this year and no doubt into 2022.

The first and most important is supply. In August only 10,609 new properties came to market. This contrasts sharply with the 18,599 that came to market in 2020. What is even more shocking is that at the end of August there were only 8,201 properties available to buyers, a 51 percent decline from the same period last year when buyers could choose from 16,662 properties. Available properties were reduced to their lowest level in over a decade. A chronic problem has now become critical.

The critical nature of the supply problem is glaringly evident in certain sub-sectors of the marketplace. At the end of August there were only 337 semi-detached properties available for sale in the entire greater Toronto area. This number is shocking but becomes eye-popping when it is remembered that in August 750 semi-detached properties were reported sold. That means that we enter September with 55 percent fewer semi-detached properties available for sale than the total number reported sold in August. Only the City of Toronto’s central districts have more semi-detached properties available at the beginning of September than sold in the month of August, and only marginally at that.

These numbers make it clear that during the current election campaign, the only housing item on all parties platforms should be supply! Platforms that speak to making purchasing properties easier – ie. longer amortization periods, government assisted loans, reducing mortgage insurance premiums, tax free home buying savings accounts – are misleading at best and reckless at worst. They are blatant, unhelpful, self- serving promises that hope to pave the way to being elected. Supply and ways to achieve it should be the only words uttered by politicians at this time.

The second theme that emerges is the disparity between the 905 region marketplace and the City of Toronto (416). The pandemic and its impact on the house buying consumer has been dramatic. Before the pandemic house prices (on average) were lower in the 905 than in the City of Toronto, nor did house prices rise as quickly in the 905 region. That has all changed.

In August the average sale price for the 905 region was more than $1,050,000. In the City of Toronto it was $1,000,000. Prior to the pandemic these differences were reversed. Also, the increase in average sales prices was more startling in the 905 region than in the City of Toronto. In the 905 region detached properties increased in value by 26 percent, semi-detached by 21 percent, townhomes by 20 percent and even condominium apartments increased by almost 15 percent. By contrast in the City of Toronto detached properties only increased by 11 percent, semi-detached by 4 percent, townhouses by 8 percent, and condominium apartments sales prices by 7 percent.

The explanation is three fold. Firstly there is less supply in the City of Toronto, except for condominium apartments, house prices are still pricier in the City of Toronto, and the pandemic, which has intensified the need for space and safety, coupled with the ability to work remotely, has driven buyers to the suburbs and secondary markets.

The third theme that has emerged is the plateauing of average sale prices. Yes, August’s average sale price of $1,070,911 for all properties sold was 12.6 percent higher than the average sale price achieved in August 2020 ($951,219), but it has steady declined since May’s stratospheric record breaking average sale price of $1,108,362 and has stabilized at approximately $1,073,000.

Without a mortgage interest rate decline, which is unlikely, or massive increase in household incomes, also unlikely, consumers have reach their maximum housing purchasing power, outliers excluded.

The last theme that is emerging is the resurgence in condominium apartment sales. During the early months of the pandemic condominium apartment sales and prices collapsed. The density of condominium living and fear of the Covid-19 virus drove consumers to ground level properties, especially in the suburbs and secondary markets. Not only were properties less expensive in the 905, and in secondary markets, those prices got consumers more space and the psychological benefit of safety.

August’s results have made it clear that the condominium apartment market is back. In the City of Toronto condominium apartment sales increased by more than 13 percent. Almost 1,740 apartments traded hands, representing almost 58 percent of all properties reported sold in the City of Toronto in August. All condominium apartment sales took pave in only 21 days at 102 percent of their asking price. In Toronto’s central districts, where most sales take place, the average sale price came at $783,712, a number beginning to exceed pre-pandemic levels. Not only are condominium apartment sales robust, but on the supply side they are practically the only game in town. At the end of August, there were 3,577 condominium apartments available to buyers. This, shockingly, represents 44 percent of the total available supply of 8,201 properties of all types.

These themes – supply, disparity between the 905 and City of Toronto marketplaces, the stabilization of average sales prices, particularly in the City of Toronto, and the resurgence of the condominium apartment market – will play out in September, similarly to how they did in August. The result will be sales results and average sale prices similar to what were achieved in August.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

In some ways the July resale market’s performance was anticlimactic. We could see it unfolding in June, and as a result, there were few surprises. Sales continued their decline – in June 11,106 properties were reported sold, dropping to 9,390 in July, but still a strong month by historical standards. The record for reported sales was established last July at 11,081. At the end of the day there are only so many buyers in our given geographical area, and since the beginning of 2021, almost 80,000 properties have changed hands, a pace that will see at least 120,000 sales take place by the end of the year, shattering the previous record of 113,400 sales achieved in 2016.

All market indicators continue to point to a very robust market. The market’s slow down is due to absorption, seasonal change, and with higher vaccination rates and declining social restrictions consumers are focusing on activities other than buying and selling real estate. In addition, even if there was no change in buyers’ attitudes, there simply isn’t enough inventory in the marketplace. In July only 12,551 properties came to market, 31 percent fewer than the number that came to in market last July. As we enter August there are only 9,732 properties available for sale in the entire greater Toronto area, more than 35 percent less than were available last year (15,018).

The sales that took place were at lightning speed. In July all 9,390 reported sales took place (on average) in only 15 days. Last July, which was a record-breaking month, they took place in 17 days. These sales also came in at record-breaking average sale prices. In July the average sale price for all properties sold was $1,062,256,12.6 percent higher than last July’s average sale price ($943,594).

A closer examination of July’s average sale price indicates the growth in sale prices is taking place in Toronto’s 905 region, and very moderate price growth in the City of Toronto, as the chart below clearly indicates, the reason for this dramatic differentiation is twofold.

Firstly, prices for homes in the 905 region are substantially lower than in the City of Toronto. Affordability is very much at play in the decision-making of buyers. Secondly, the need and desire for more space and perceived more safety, continues to drive buyers away from dense areas in Toronto to the less crowded suburbs. Of the 9,390 reported sales in July, 6,121 traded in the 905 region, or more than 65 percent. This trend is not likely to end soon.

Overall, the high end of the market continues to perform very strongly. In July 521 properties having a sale price of $2 Million or more were reported sold. Last year only 452 properties were sold in this category of homes. It is amazing to look back to 2019. In that year only 185 properties were bought and sold having a sale price of $2 Million or more. In just two years the number of high-end properties sold has increased by an eye-popping 182 percent.

Condominium apartment sales have continued to strengthen over the last few months, particularly in the City of Toronto, where the availability of most condominium apartments is located. In fact, in July condominium apartments were the only housing type that saw year-over-year growth, with detached, semi-detached, and townhouse sales all producing negative variances compared to July of last year. Condominium apartment sales were up by 4.2 percent.

July saw the first overall negative variance in sales in 12 months. Again, it must be remembered that reported sales in July 2020 were record-breaking. Last July 11,033 properties were sold, this year 9,390. July was the fourth straight month of declining sales, which as discussed in our June market report, was anticipated, for reasons already stated – absorption, affordability, lack of supply, and historic seasonal adjustment. Early indications are that this trajectory will continue into August, and for the same reasons. Last August 10,738 residential resale properties were reported sold. This August we will see close to 8,500 properties trading hands. This does not mean that the market is softening. In 2019, which was a solid resale year, 7,682 properties were reported sold. What we are witnessing is the resale market slowly morphing back to pre-pandemic patterns.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

There were 11,106 resale properties reported sold in June in the greater Toronto area. In the City of Toronto 3,850 properties changed hands. In both areas, these numbers were substantially lower than the astronomical peak achieved in March. Having said that, sales activity in June was only outpaced by June sales achieved in June 2016.

The Toronto and area market remains very strong, even though it may feel like it has softened. Peak momentum is clearly now behind us, although some components of the marketplace – ie. condominium apartments and various sought-after neighbourhoods – may resist both the softening of sales and average prices.

In June the average sale price for all properties sold came in at $1,089,536, 17 percent higher than the price for properties sold last year ($931,131). Because the City of Toronto’s numbers are heavily weighted by condominium apartment sales, the average sale price for the City was a little lower at $1,079,749.

Detached and semi-detached property prices in the City remained very robust at $1,700,000 and $1,267,000 respectively. Detached properties increased by 11.5 percent compared to last year, while semi-detached sale prices actually declined by almost 2 percent. This decline was due more to lack of supply than demand.

The high end of the market continued to perform robustly in June. This year 699 properties having a sale price of $2 Million or more were reported sold. Last year only 365 properties were reported sold in this price category, in percentage terms, an increase of almost 92 percent. With an increase in the average sale price of 17 percent, and 2,461 more properties reported sold this June, it is not surprising to see more property sales in the $2 Million plus range. Most of the greater Toronto area property sales are now in the $1 Million to $1.5 Million range.

Price increases were eye-popping in the 905 region. Detached property sale prices increased by almost 30 percent to $1,329,873, while semi-detached property prices increased by 21.5 percent to $915,000. These increases reflect the fact that buyers are continuing to flock to less expensive, ground-level homes, in less dense neighbourhoods. This phenomenon was dramatically accelerated by the concern for space and security (and price) generated by the pandemic.

Condominium apartment sales momentum continued in June, a pattern that first became noticeable at the beginning of this year. During the initial months of the pandemic and for most of 2020, condominium apartment sales fell off a cliff, victim to buyers’ quest for ground-level properties offering more space and security. In June 2,800 condominium apartments were reported sold in the greater Toronto area, a 57 percent increase compared to June last year. Most of those sales were in the City of Toronto (1,901).

With the increase in sales, prices have also been increasing. In June average sale prices for condominium apartments reached pre-pandemic levels. The average sale price for sales in the City of Toronto reached $717,466. In Toronto’s central districts where most condominium apartment sales take place (1,247) the average sale price rose to $770,000. Not only did the average price reach these lofty levels, but all central Toronto sales took place (on average) in only 15 days and at 102 percent of the list price. Buyers are fearlessly returning to high rise living.

Throughout the heady pandemic market supply has been a problem. There was no relief in June. Only 16,189 properties came to market, almost the exact number that came to market last year. Unfortunately, due to the extraordinary absorption in sales that have taken place in 2021, we enter July with only 11,297 properties available to buyers, almost 20 percent fewer than were available last year at this time.

Early July market data indicates that the pace of sales and the average sale price for properties sold will continue declining. July’s market will be primarily impacted by seasonal influences and consumers’ return to more “normal summer” activities. The province has been in lockdown for many months. The lifting of restrictions is beginning to moderate the consumer’s fixation for engaging in real estate buying and selling.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

The Toronto and area residential resale marketplace continued its slide towards a more normal but still very strong market. In May 11,951 properties were reported sold, a decline of more than 12 percent compared to the 13,650 properties reported sold in April, and a decline of more than 23 percent compared to the record breaking, stratospheric 15,646 properties sold in March. March’s numbers were, I believe, the zenith of the pandemic market, just before Ontario’s vaccination program was rolled-out.

I reiterate, that notwithstanding these declines, the market remains very strong by historic standards and May’s average sale price of $1,108,453, which includes more than 2,700 condominium apartment sales throughout the region, is an all-time record. May’s average sale price was almost 30 percent higher than last May’s average sale price of $863,583. In absolute dollars, a stunning increase of $245,000 in just 12 months. This record-breaking average sale price is clearly stretching the affordability limits of Toronto and area buyers.

Although the number of sales declined over the past two months, the pace of sales did not. In May it took only 11 days for all properties that came to market to be reported sold. At the end of May there were only 1.2 months of inventory for the entire greater Toronto region. The number was a little higher in the City of Toronto (1.6 months) due to the preponderance of condominium apartments in the City.

Condominium apartment sales have surged during 2021, and although comparison to 2020, at least until the month of June are not meaningful, in May the 1,881 condominium apartment sales recorded in the City of Toronto were almost 160 percent higher than last May’s results. With this surge in sales, sale prices for condominium apartments have also increased. The average sale price for condos in the City of Toronto came in at $716,976, a 6.3 percent increase compared to last year. In the City’s central core, where most of the region’s condominium apartments are located, the average sale price came in at $766,462, making Toronto’s least expensive housing form fairly pricey.

The price of detached and semi-detached property sales in the City of Toronto reached eye-popping levels in May. The average price for detached properties came in at $1,716,272, and $1,326,153 for semi-detached properties, increases of 20 and 16 percent respectively compared to last year. Average sale prices in the 905 region were not as high – $1,331,176 for detached properties, and $915,479 for semi-detached homes – however, from a percentage standpoint they exceeded the increases in the City of Toronto. In the 905 region detached property sale prices increased by 41 percent while semi-detached increased by 28 percent over the same period last year, a reflection of buyers fleeing to the suburbs, seeking more space and a sense of safety, at prices for less than can be found in the City of Toronto.

Affordability and supply will continue to moderate the Toronto and area marketplace as we move towards the second half of 2021. The region’s average sale price of $1,108,453 is making Toronto and area very pricey, and except for condominium apartments, beyond the reach of most buyers. To some extent that has been one of the reasons for the pull back in the market since March. Affordability will become even more relevant as the higher mortgage stress tests are applied beginning in June.

In May 18,586 new listings came to market. Sellers were clearly taking advantage of the record-breaking selling prices. The growth of the Toronto and area inventory levels will have a moderate impact on average sale prices, as stretched buyers discover that they have more choice than during the early months of 2021. The combined impact of tighter affordability and more inventory should see the marketplace continue to level off, consistent was “normal” pre-pandemic markets.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

Market reports rely heavily on comparisons to the same month the year before. Comparing April 2021 to April 2020 would be pointless. Last April we were in the darkest period of the Pandemic. Buyers, sellers, and their realtors were developing and adapting to new, restrictive, and demanding industry protocols. As a result, there were fewer properties available for sale and even fewer sales. As a result, it is much more fruitful to look at what unfolded just this past March and compare it to April’s market performance.

March 2021 was an all-time record breaking month both for the number of properties reported sold and the average sale price. April 2021 could not keep pace with the torrid March market. Having said that, April was itself record breaking, setting a new record for reported sales for any previous April. There were 13,663 homes reported sold, 12 percent fewer than the blistering 15,652 that were sold in March. There was also a marginal decline in the average sale price. March’s average sale price came in at $1,097,565. Although still eye-popping, April’s average sale price dipped to $1,090,992.

The decline in price was across the board for all housing types, except condominium apartments. Detached, semi- detached, and townhouse property prices all declined, albeit marginally. In April the average price for detached properties came in at $1,699,756 (a 3 percent decline from March), semi-detached at $1,288,005 (a 1.5 percent decline), and townhouses at $942,371 (a 2 percent decline).

The outlier was condominium apartment sale prices. In April 3,290 condominium apartment sales were recorded, a considerable decline from the 3,821 reported sold in March, a decline of almost 14 percent, contributing substantially to the overall decline in market sales as compared to March. However, while sales declined, prices increased, both in the City of Toronto and the 905 region. The average sale price for City of Toronto condominium apartments came in at $727,137, up from the $707,835 achieved in March. In Toronto’s central districts, where most of the greater Toronto’s condominium apartments are located, the average sale price came in at $781,471, a number not far off average sales prices for condominium apartments pre the Pandemic.

So, what does all this data tell us about the Toronto and area marketplace? Firstly, it was impossible that March’s pace could be exceeded or even equaled for a second month in a row. Since the beginning of 2021, 47,157 properties in the greater Toronto area have changed hands. Historically this is an unprecedent pace. What April’s data tells us is there has been tremendous buyer absorption during the last few months of 2020 and now into the first four months of 2021. Bluntly, the market is running out of buyers. With no immigration since last March, and with many city dwellers moving to secondary markets during the Pandemic, the number of potential buyers is declining.

As to the average sale price, it appears that it too may have reached a pinnacle in March. Between 2019 and March 2021, average sale prices have increased by more than 20 percent. Household incomes have not. A recent study indicated that the decline in mortgage interest rates over the same period has boosted the price that buyers could pay for properties by 22 percent. It is not coincidental therefore that average sale prices have increased by more than 20 percent over the same period.

Subject to an increase in migration to the Toronto area from other parts of the country and a return to pre-Pandemic immigration levels, the market has probably plateaued and in fact we may see a slight decline in sales as we make our way to the latter half of 2021. Similarly, unless there are declines in mortgage interest rates, the average sale price has plateaued at approximately $1,100,000. Looming on the horizon is the more restrictive mortgage stress testing effective June 1, 2021, which will place further restrictions on buyers’ borrowing power.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

Just when you think the Toronto residential resale market can’t reach new heights, it surprises us again. March was not only strong but it shattered records, something that is becoming a common occurrence.

In March 15,652 homes were reported sold, an all-time monthly record and 97 percent more than the 7,945 properties sold last March. Even considering that the second half of March 2020 was impacted by the implementation of Covid restrictions, March’s results are nothing but extraordinary.

Not only was sales volume record-shattering, but so was the average price. The average price for Toronto and area came in at an eye-popping $1,097,585, the highest average sale price ever recorded. This number is even more impressive when it’s remembered that it included the sale of almost 4,000 condominium apartment units, the least expensive homes on the market, averaging less than $700,000.

The average sale price was unequivocally driven by the unbelievable number of high-end properties that were reported sold. In March 982 properties having a sale price of $2 Million or more changed hands – also a record! By comparison, only 245 sold in this category last year, obviously a number dampened by the effects of the pandemic’s restrictions during the last half of the month.

The speed at which properties sold was also record-breaking. All 15,652 properties reported sold in March came to market and were sold in only 13 days. There are no market descriptors that can define this phenomenon. At one time it was the eastern trading districts in Toronto, in particular Riverdale, Leslieville, and the Beaches, that had speed of light sales. Now sales are taking place even in the 905 region at an incredible pace.

Not only are properties selling quickly in the 905 region, but they also account for the bulk of all reported sales. Of the 15,652 sales in March, 10,522 of them took place in the 905 region, representing 67 percent of all reported sales.

In March condominium apartment sales continued a resurgence that began at the end of 2020. Condominium apartment sales increased by 87 percent in the City of Toronto and by 100 percent in the 905 region compared to last year. Although average sale prices increased in the 905 region by 13.5 percent to $607,000, they remained flat in the City of Toronto at $707,000.

March had a bright spot for stretched and frustrated buyers. In March 22,709 properties came to market, a much-needed increase in inventory, and 57 percent more than March of last year. It would appear that sellers are becoming eager to capitalize on the incredible prices that were achieved this month.

This runaway market gives rise to a variety of issues. There is the issue of sustainability. The average sale price reached a lofty $1,097,565 in March, almost $200,000 higher than it was a year ago. Average household income has not increased proportionately. Far from it. Even more worrisome, at the date of preparation of this Report, (April 8th), the average sale price in the City of Toronto was even higher at $1,106,000, including condominium apartment sales.

When the sustainability of the housing market becomes an issue, it generates government scrutiny. Government intervention inevitably leads to unwanted consequences, as past government intervention has clearly demonstrated. So there is talk of a capital gains tax on principal residences and even a speculation tax. The best solution is an organic one – namely the market moderates itself because households become incapable of paying higher prices, and more inventory comes to market. We are beginning to see signs of both of these developments.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.

Is it really February? The Toronto and area residential resale market certainly did not behave as if it was. Actually, it was more reminiscent of a crazy spring market, and even then, it outdistanced most spring markets that we have recently experienced. In February 2021, 10,970 properties were reported sold in the greater Toronto area. To put that number into perspective, no month in 2019 came close to 10,970 sales. The strongest month for sales in 2019 was May at only 9,951 reported sales, and that was an excellent month! By comparison to February 2020, also a strong month at 7,193 sales, February 2020’s performance was 52.5 percent stronger.

It will surprise no one with such robust sales activity that prices were also sharply on the rise in February. In fact, the average sale price for the greater Toronto area shattered the $1 Million threshold for the first time, finishing the month at $1,045,488, almost 15 percent higher than the average sale price of $910,142 achieved last year. It is interesting to note that the average sale price for the City of Toronto came in lower at $995,201. That was due to the 2,167 condominium apartment sales that were recorded. These lower price point properties acted as a drag on the City of Toronto average sale prices.

Detached and semi-detached property sales in the City of Toronto were extremely active and at a strong prices. Expect to pay almost $1.7 Million for a detached property and $1.325 Million for a semi-detached home – if you can find one. The supply of detached and semi-detached properties in Toronto is at an all-time low. In February, 915 detached properties were reported sold. By March, the inventory of detached properties was down to 938 homes or only 1 month of supply. The supply of semi-detached properties has reached a critical state. In February, 295 properties sold in this category. By the beginning of March, only 181 semi-detached properties were on the market, only .6 months of supply – an unprecedented number.

Sales of every housing type, including condominiums, were strong. This was particularly true for higher-priced properties. In February, 597 properties having a sale price of $2 Million or more were reported sold. Comparisons to previous years are staggering. In 2020 only 266 properties in this price category were sold, and in 2019 a mere 193. Sales in February 2021 were a shocking 125 percent higher than sales at this price point in 2020.

Condominium apartment sales were also very strong in February, posting results 63.2 percent higher than last year. While sales increased, the average sale price continued to decline by 6.4 percent in Toronto but rising by 5.4 percent in the 905 region. It is the decline that is relevant in that 70 percent of all condominium apartment sales are in the City of Toronto. The decline in average sale price in the City’s core, where most sales are recorded, was even lower, down by 10 percent compared to last year.

February’s resale market was like no other we have experienced. Going forward we can anticipate more of this, at least until March and into April, however sustaining 15 percent price increases (higher in some districts) will be difficult. Even with historically low mortgage interest rates, affordability will become (is?) a concern. On the positive side, February saw new inventory increase by over 40 percent compared to last year. If the pace of new listings coming to market continues, more consumer choice should see prices begin to moderate. But currently, with only 1.5 months of inventory, price moderation is still some months away.

Prepared by Chris Kapches, LLB, President and CEO, Broker, Chestnut Park® Real Estate Limited, Brokerage.

Have questions about the market or selling or buying?

Contact me any time. I’m happy to answer any questions you may have.